Bill, Network Effects?, and Repeat Transactions

Thanks to all who are reading this week! I'm deeply appreciative of your time. Feel free to send me any thoughts you may have on this piece, especially on network effects.

Bill, formerly know as Bill.com, simplifies financial back-office tasks for SMBs. This currently covers three different areas: accounts payable, accounts receivable, and expense management. The founder, René Lacerte, has in many ways been steeped in small business his whole life. He left his accounting job to work for his parents’ business, then joined Intuit, then started a payroll company, PayCycle, that was acquired by Intuit (although after René had left), and then founded Bill. The company went public in 2019, and opportunistically raised equity twice more after that, most recently in late 2021. It’s put some of these funds to work quickly by acquiring three different businesses:

Invoice2Go - mobile-first accounts receivable software purchased for 674mm in a mix of stock and cash. Mark Lenhard, who was Invoice2Go’s CEO at the time of acquisition, is now COO of Bill. Invoice2Go actually has more subscribers than Bill’s core business (228,500 vs 182,700) but contributes less in revenue.

Divvy - spend management software purchased for 2.3B in a mix of stock and cash. Divvy has slightly more upmarket customers than Bill and is also an earlier stage business, so growth has continued to be impressive even with the current macro environment. Revenue last quarter grew 188% YoY. Divvy’s CEO, Blake Murray, became CRO of Bill in Q22022, but is now just in an advisory position.

Finmark - financial planning software for SMBs. Terms weren’t disclosed, but Finmark is an early stage business and was acquired in November 2022, so the price paid was likely quite reasonable.

The benefit of raising all this cash during the tech bull market is that Bill is now in a favorable position for a potential economic downturn. The downside is that these raises led to significant equity dilution that’s been compounded by a generous stock-based comp program, to the tune of 300mm this fiscal year. Management initiated a 300mm stock buyback program to partially offset this dilution, but this can uncharitably be read as a tactic to make sure employees are motivated, but without the higher salaries that would impede Bill hitting non-GAAP profitability this year.1

It’s somewhat of an understatement to say Bill’s growth has been impressive: the company ended its 2022 fiscal year with organic core revenue up 77% YoY, and until this most recent quarter was seemingly constantly raising estimates.2 It’s also somewhat of an understatement to say costs have ballooned. While total revenue has grown 114% annualized from 2019-2022, total operating expenses have grown 148%, including an 130% increase in R&D and an 151% increase in S&M. The most recent quarter shows spending continuing unabated, even in the current economic climate and in stark contrast to other growth-stage software companies. It’s difficult to see heavy S&M spend coming down dramatically anytime soon as much of the increase is tied to Divvy, which offers customers generous rewards for using its expense management cards. These rewards are classified as a marketing expense, and scaling them back would save money but also cede market share to competitors like Ramp and Brex.3

A big challenge for businesses serving SMBs is figuring out a distribution model. Bill has done an exceptional job at this, which constitutes an important advantage for the company.4 It primarily sells to customers in three ways:

Directly

Through Accounting Firms. Bill offers these accounting firms wholesale pricing, which can be thought of as a kind of sales and marketing expense. This lower pricing means the partnerships represented 48% of Bill customers but 27% of revenue for fiscal year 2022.

Through Financial Institutions. Bill partners with financial institutions like American Express and Bank of America to offer white labelled solutions. These partners pay Bill contractural minimums over a multi-year period, with the opportunity for additional revenue if there’s better than expected customer adoption. These contractural minimums mean that for the time being customer growth is outpacing revenue growth. Financial institutions accounted for over half of net customer adds last quarter, but represented only 4-5% of revenue.

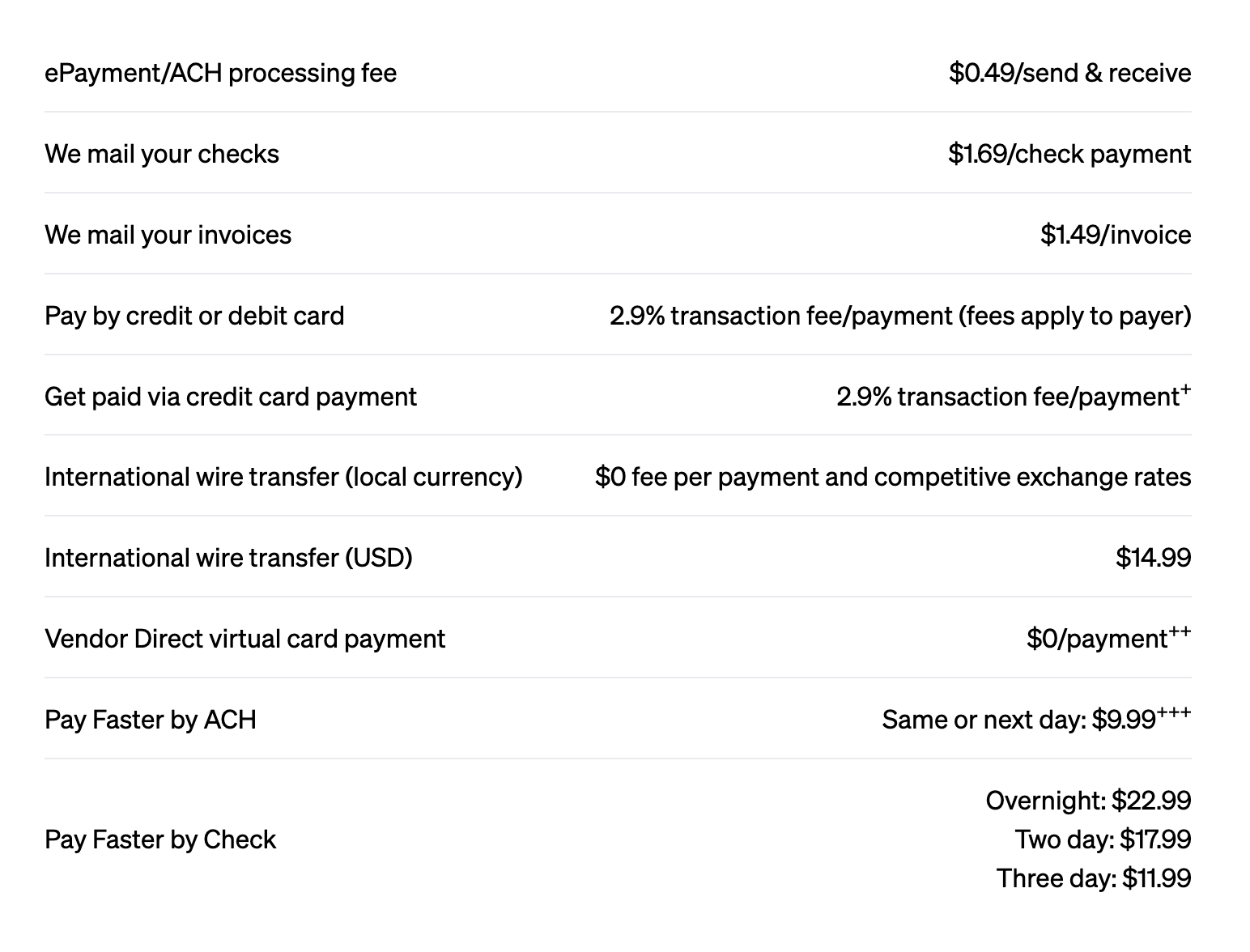

Bill currently makes money from subscriptions, transaction fees, and interest income, which makes it one of the few growth-stage technology businesses that’s actually somewhat helped by higher rates. Transaction fees make up the bulk of revenue, and last year contributed 439mm in top line as compared to 193.5mm from subscriptions and 5.4mm from interest income.5 These fees vary by transaction type, as seen below:

At this time, the vast majority of Bill’s transaction revenue comes from fixed-price products. This is beginning to shift somewhat, with variable priced payments making up 10% of TPV (Total Processing Volume) in Q4. Entertainingly, some of Bill’s work on the payments front is focused on just getting customers to switch from mailing checks and invoices to paying/getting paid via ACH. In the short term this is a drag on the business’s take rate, as seen from the prices above, but over the longer term it creates a larger opportunity for variable price payments. It’s challenging to take a customer straight from paying by check to paying by credit card; it’s less challenging if you add an intermediary step of having them pay via ACH. 15% of Bill’s payments business is still offline, so this migration is not an inconsequential opportunity.

Management is keen to emphasize two other things about its transaction business: the size of its network, which stood at 4.7mm members at the end of Q2, and the recurring nature of many of these payments. Bill defines its network members as its customers plus their suppliers and clients, and its size matters because of the network effects and potential customer pool it creates.6 The value of this network may be overstated. It’s true that customers’ suppliers/clients very often have to create a Bill account when they're paid/payment is requested, which no doubt removes some friction to converting this supplier/client to a subscriber. Additionally, the size of Bill's network does indeed create value for paying customers, who are able to search this network for suppliers/clients they may need to interact with. The larger the network, the more valuable this search function becomes. That being said, Bill's core subscription business sits at 182,700 customers as of Q2. In other words, there are 4.5mm non-paying members who are not able to search Bill’s network, and so derive little value from its size. Consequently, it would be a mistake to conclude the size of Bill’s network creates the same amount of value, or the same moat, that Cash App’s or Venmo’s does. That’s not to say Bill doesn’t have customer lock in, its recurring payments and impressive NDR figures are evidence that it does, but it is to say the network may not be a substantial moat.7 This will become even more true as Bill tries to shift more of its payment’s business to variable priced products like credit cards. Paying via ACH requires creating a Bill account, but when a customer’s client pays via credit card he just has to enter his card info. Such a client is now technically part of Bill's network, but without an account he's not searchable, and so while he improves Bill's payments revenue and margins he doesn't increase network value even for paying subscribers.

While Bill’s network may not be a significant strength, the recurring nature of its customers’ payments likely is, and is something consumer payment networks would struggle to brag about:

“Much of our revenue comes from repeat transactions; in fact, repeat transactions by our customers are an important contributor to our recurring revenue: approximately 80% of both the Total Payment Volume (as defined below) and the number of transactions on our platform in every month of fiscal 2019 represented payments to suppliers or from clients that had also been paid or received by those same customers in the preceding three months.” - Pg 64, Bill S1 filing.8

There are two arguments for why the recurring nature of these payments matter. The first is that Bill’s aiming to be the financial nervous system for SMBs, and part of succeeding at this is making sure customers aren’t primarily using the platform for one time payments. Repeat transactions to the same suppliers/clients are a good indication that Bill’s become embedded into its customers’ workflows. The second, more tenuous, argument for the importance of recurring payments is that it means 80% of Bill’s payment revenue can be viewed as guaranteed, much like subscription revenue. This is a stretch. Repeat transactions with customers’ suppliers/clients do lend a level of stability to the business, especially in the form of lower customer churn, but it’s incorrect to think of these transactions as having reliable dollar amounts. This was apparent on Bill’s most recent earnings call, where management forecasted that Bill’s standalone TPV growth would be flat YoY for the upcoming quarter.9 Given that there will be subscriber growth, this implies that existing customer TPV will actually be down YoY.10 It is of course valuable to be handling customers’ payments to suppliers/clients, but there’s a danger in assuming that this payments revenue can be thought of as part of ARR.

Organic core revenue is defined as revenue excluding Invoice2Go and Divvy.

More info on this can be found on page 10 of Bill’s 2021 Annual Report.

a16z has a piece on Bill’s distribution advantage here. I think it’s overly optimistic on the strength of Bill’s network, but it’s a good read nonetheless.

This was not the case at the time of IPO, when subscription revenue was greater than transaction revenue.

See pg 4 of Bill’s 2021 Annual Report for more info.

NDR for fiscal year 2022 was 131%, which is up from 124% in ‘21, 121% in ‘20, and 110% for 2019.

To my knowledge Bill hasn’t updated this figure. Its most recent annual report was more vague than the S1: “Much of our revenue comes from repeat transactions, which are an important contributor to our recurring revenue”(56).

Standalone TPV is TPV excluding Divvy.

Samad Samana from Jefferies brought this up on Bill’s most recent earnings call.