Blackstone: A Test in Generating Alpha at Scale $bx

Perpetual Capital, Private Credit, and the Power of a Brand Name

The life of an asset manager seems to follow an arc in where one increasingly appreciates the advantages of Berkshire Hathaways’s business model. While it was probably difficult to deal with negative press during periods of underperformance, Buffett didn’t have to worry that his insurance float would suddenly suffer from short-termism and pull money overnight.

Private equity funds at least somewhat solve the problem of investors acting in their short-term interests to their detriment of their long-term ones. No matter how poor a fund’s performance might be in any given year, a multi-year lockup is a multi-year lockup. There are, however, a few drawbacks to this model. The first is that, in addition to your track record, raising another fund is inevitably influenced by the macro/fundraising environment of that point in time. The second is that a big chunk of compensation comes from realized gains once an investment is sold or goes public. These gains take time to materialize and are inevitably lumpy in nature. That’s not necessarily ideal as the partner of a privately held investment fund, but it’s even less ideal as the partner of a publicly traded one. When a chunk of a employee compensation is tied to a company’s share price, the market’s perception of that company as lumpy/difficult to forecast is going to cause the company to look for fixes to that perception.

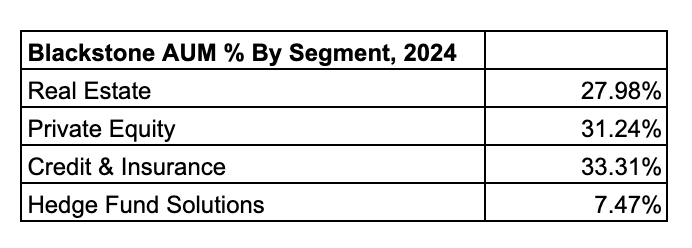

Blackstone, a name synonymous with private equity, is a company that’s done just that. The firm was founded in 1985 as an M&A advisory business, and from there expanded into private equity, hedge funds (including a fund of funds), real estate, and credit.1 It makes money, as all private equity firms do, by charging both a management fee that’s a percentage of assets and a performance fee for returns above a certain hurdle. (Note: Blackstone manages assets on behalf of insurers within its credit portfolio. It doesn’t itself operate an insurance business).

Increasingly, Blackstone has been raising money for what it terms “perpetual capital” vehicles. These vehicles span all of Blackstone’s business segments, and can be broadly split between offerings for retail investors and offerings for institutions. Blackstone caps redemptions for its perpetual retail products at a certain percentage of net asset value per month, and institutions can’t redeem capital from these vehicles unless new capital comes in to fill their gap. Given that these funds are perpetual, performance fees are charged on unrealized, rather than realized gains (these fees are defined as “fee related performance revenues” when Blackstone reports earnings.) The frequency of these performance fees vary (As examples, BREIT, Blackstone’s real estate product for retail investors, charges performance fees once a year, Blackstone’s Infrastructure fund for institutions charges performance fees every three years). Today, perpetual capital under management sits at 444.8 billion, or ~40% of overall assets.

It’s worth exploring the challenges that these perpetual capital vehicles do and do not solve. They do mitigate the vicissitudes of the fundraising cycle and they do mean that Blackstone has a more stable stream of income. That said, there’s still a large amount of variance in those recurring streams. As a case in point, fee related performance revenues for the company’s real estate segment were up 401% from 2020-2021, then down 37% from ’21 to ’22, down another 73% from ’22 to ’23, and then down a further 31% from ’23 to ’24. Performance fees work well when the underlying funds perform well, but less well when the funds don’t! Moreover, perpetual capital vehicles are unfortunately not able to totally prevent investors pulling money over short-term performance concerns. When BREIT withdrawals picked up in late 2022 to more than 2% of NAV per month, the company announced it was limiting withdrawals (something it is very much allowed to do!). This is turn caused increased media coverage, a drop in Blackstone’s share price, and further requests for withdrawals that exceeded the 2% NAV limit until April 2024.

The life of an asset manager also follows an arc where one typically generates less alpha as fund size becomes larger. There are multiple possible explanations for this, but the explanation based purely on AUM growth rather than the portfolio manager now having enough money that he/she no longer cares as much about performance is that a larger fund size just makes deploying capital harder. This is most clearly the case with a successful microcap public equities investor: part of the reason microcaps are such an inefficient space is because most funds are too big to justify spending any time looking at companies with a sub 250mm market cap. A microcap manager whose fund grows in size must now spend his/her time looking at a basket of stocks that are much more efficiently priced, so substantial outperformance becomes a lot harder.

Given that its AUM now sits at over a trillion dollars, Blackstone has had to think about the trade-offs between fund size and performance more than most. Management argues that its scale confers a few advantages:

1. It can be one of the only seats at the table for extremely large deals.

2. There’s a lot of cross pollination that can happen across business segments. The real-estate teams can talk to the hedge fund teams can talk to the infrastructure teams, etc etc. This leads to insights that a single asset class firm wouldn’t uncover.

There’s a real question as to whether being one of the few seats at the table is always an advantage. You’re able to do deals that few investors can do, but that means there are few investors at the table when you try to exit an investment, which becomes an especially acute problem when the IPO market is tepid. Nonetheless, there do seem to be market segments, such as healthcare, where Blackstone’s size confers true benefits. Its pure life sciences business began in 2018 with the acquisition of Clarus, and is primarily focused on “financing the last mile of clinical development of pharmaceutical products.” In other words, Blackstone is funding things like drugs in phase 3 clinical trials, where the science risk has been significantly reduced but there’s a substantial funding need. There’s a considerable supply/demand gap in life sciences R&D, so it’s a space where Blackstone’s scale means it’s one of the few seats at the table and that it’s meeting a funding need that wouldn’t be met otherwise. The exit opportunities are also different. The downside of Blackstone being one of the few seats at the table for a private-equity deal is that there are then only a few seats at the table when Blackstone wants to exit this deal. On the life sciences side, however, the exit opportunities are more binary and less subject to market conditions. If the clinical trial/insurer reimbursement process is a success, Blackstone makes a lot money. If the clinical trial or reimbursement process isn’t a success, then Blackstone makes very little. The cross-pollination opportunities in life sciences are very real. Blackstone owns a significant amount of life-sciences real-estate (although that’s been a performance headwind as of late!), and has purchased two clinical trials related businesses out of its private equity funds. That’s not to say cross-pollination doesn’t have its downsides – if Blackstone gets its AI bets wrong its real-estate funds (via data-center investments), infrastructure funds (via data-center and power generation investments), and private credit funds (via its financing of CoreWeave) will all suffer.

There’s a third advantage to Blackstone’s scale that is the most relevant to its business going forward: it enables the long-term growth of its private wealth and insurance/credit segments. Historically, private wealth has been under allocated to private markets when compared to institutional money (Blackstone quotes that institutional investors are 30% allocated as compared to private wealth’s 1-2%). Some of this difference is structural: Wealthy families and individuals have greater liquidity needs than a university endowment! Even so, a portion of this difference is because there hasn’t been an easy way for individuals below a certain net worth to invest in privates. Consequently, Blackstone’s put an enormous number of resources into developing this business, an effort that began well before its competitors in 2011. There’s good reason to think the firm is exceptionally well positioned to succeed here, as management has pointed out:

“I think the one advantage, I’d say in this [the private wealth] market versus the institutional market, there you can have thousands and thousands of individual private equity firms or real estate firms, credit firms. I think when you get to private wealth, the brands are going to matter, the scale, the ability to service. And I think it’ll be a smaller number of players in that segment. It’ll grow over time, but it requires something different. And we have a pretty meaningful first mover advantage, $240 billion of total assets, and we are absolutely committed to delivering great performance and great service to the underlying customer. So, we recognize it’s going to be more competitive. Others will try to do things in the marketplace.”2

If you’re a small private equity firm, it just doesn’t make sense for you to spend time building out a private wealth segment. Not only are you unlikely to have the capital or patience or distribution know how to build relationships with a substantial number of financial advisors or navigate regulatory hurdles, but you don’t have a sufficiently recognizable brand name. Even if there were no distribution/regulatory challenges to figure out, there’s little reason for an advisor to recommend an unknown fund to its clients. “No one ever got fired for buying IBM” can easily be changed to “No one got fired for investing in Blackstone.” Moreover, Blackstone’s existing private wealth presence means it’s relatively easy to raise money for any additional funds launched in this channel: BXINFRA, its infrastructure product for private wealth, launched with over 5x the assets of its competitors’ products, and “over 90% of advisers who allocated to this strategy had previously allocated to another Blackstone perpetual vehicle and over 50% allocated to all 4 of our perpetual flagships.”3 It’s hard to imagine a scenario where a shift in private wealth allocations towards illiquids doesn’t end up seriously benefiting all the large players, but especially Blackstone given its early start. I think this holds even if fund performance dips somewhat (although there’s obviously a limit to this). The private wealth category is essentially a way for Blackstone to convert its years of generating alpha for institutions into an ‘alpha-lite’ product serving a massive TAM.

There are similar dynamics present in Blackstone’s insurance business, which now sits at 230 billion in assets. Blackstone itself is not an insurer (unlike Apollo, which owns Athene), but instead manages money on behalf of insurance companies. Importantly, this insurance money is the stickiest of any money Blackstone manages:

“Investment advisory agreements related to certain separately managed accounts in our Credit & Insurance and Hedge Fund Solutions segments, excluding our separately managed accounts in our insurance platform, may generally be terminated by an investor on 30 to 90 days’ notice. Separately managed accounts in our insurance platform can generally only be terminated for longterm underperformance, cause and certain other limited circumstances, in each case subject to Blackstone’s right to cure.”4

While this money is sticky, it’s invested in Blackstone’s credit strategies, and so is lower fee. These lower fees end up as an advantage. For managing insurer’s money to be worth the squeeze you need two things: the ability to manage truly massive amounts of capital, and the ability to originate not only a substantial volume of private credit deals but a volume of high-quality private credit deals that will actually generate outperformance. Said differently, this just isn’t a business line that an average private equity or private credit firm can decide to get into, no matter how much excitement there may be about the asset class in general! Brand name (and the firm’s longevity) is vital here, too. Insurance is not a business where one is supposed to take large amounts of risk! Like private wealth, this is a case where it’s just not worth taking the career risk to invest an insurance company’s capital in an upstart private credit firm.

The big risk that Blackstone and the other dominant players face with private credit is that success in the business is reliant upon the amount you can originate. This creates a natural incentive to let origination quality suffer in the name of growing assets, a strategy that will fare especially poorly when managing money on behalf of the insurance industry.5 This incentive only increases as the asset class gets more competitive, a dynamic that is very much present now! In the past few months, Blackrock spent 12 billion to acquire HPS, JP Morgan announced it would invest 50 billion of its capital in private credit deals, and Goldman CEO David Solomon said private credit was “one of the most important structural trends taking place in finance.” Long-term underperformance has very real implications for insurers, and the end result of a decline in private credit performance is that they get spooked and pull money once they can.

It's a shame I didn’t write this note back when in 2012, when Blackstone was trading at 10x earnings rather than the ~43x it trades at today. There’s of course much to like about the business. Schwartzman refers to Blackstone as “the reference firm in our industry”, which really is true. Jonathan Gray, the firm’s COO, described much of its strategy as a “commitment to our capital-light, brand-heavy, open architecture model.”6 In other words, an approach similar to a former portfolio company, Hilton. Blackstone’s reputation gives it a tremendous advantage in growing its private wealth, insurance, and more traditional business segments. Its move towards perpetual capital means that a significant portion of revenue is at the very least recurring-ish. That doesn’t however, mean that the firm isn’t quite dependent upon the overall macro environment for its performance, and, as seen above, that both management and performance fees don’t drop dramatically (and for a prolonged period, which inevitably impacts fundraising in those years) when portfolio performance is poor. If the macro over the next year is smooth things probably look very good: real-estate performance improves, private wealth doesn’t get spooked, defaults stay low so money keeps coming into credit, and the IPO market opens up again so realized performance revenues soar.7 This could very well happen, and I don’t doubt that private wealth and private credit are huge opportunities. But I do wonder whether 43 times earnings is the right price to pay for a business that can have large amounts of lumpiness should the macro go south.

Disclaimer: The information in this post is not intended to be and does not constitute investment or financial advice. You should not make any decision based on the information presented without conducting independent due diligence

Funnily enough, Blackstone was actually an early backer of Blackrock, and sold its stake far far too early in ‘95 (a mistake Schwarzman described as his worst business decision ever). It’s entertaining to think of Blackstone’s fund of funds as basically an attempt to remedy this mistake.

Taken from Blackstone’s Q2 2024 Earnings Call.

Q4, 2024 Earnings Call.

Page 5, 2023 Annual Report.

For a scathing critique of private credit as an asset class, check out Dan Rasmussen’s piece for Institutional Investor.

Q3 2024 Earnings Call

There’s a funny argument that this would actually be bad for Blackstone, depending on how much of its private credit business is used to fund dividend recaps for PE funds that need to return capital to investors but have limited liquidity options.