Krispy Kreme, the Hub and Spoke Model, McDonald's, and Net Leverage

Thanks to all who are reading this week! I'm deeply appreciative of your time.

In 2016 Krispy Kreme was taken private by JAB, a holding company that invests in consumer goods and services businesses. Krispy Kreme spent the next 5 years rethinking its business strategy, and then went public again in the summer of 2021. Its pivot was well defined in the company’s S1:

“Since the JAB Acquisition, we have transformed our business and re-focused our strategy to grow our presence and expand our consumer reach. This is exemplified by the development of our omni-channel business model, which levers our Hot Light Shops to provide an experiential consumer experience and produce doughnuts for our fresh retail, DFD,1 e-Commerce and delivery, ensuring that our consumers are able to access our products in numerous ways………. Over the past few years, we have started to fully transition to a DFD model that is enabled by our Hot Light Theater Shops and Doughnut Factories. We have also introduced our Branded Sweet Treat Line offered through grocery, mass merchandise and convenience retail locations, which launched in mid-2020. We believe the transformed DFD model and new Branded Sweet Treat Line provide a superior customer experience and has led to greater demand from our retail partners and higher sales per DFD point of access.”

Over the years Krispy Kreme has suffered from a somewhat bizarre problem that helps explain the shift to omni-channel: customers love their doughnuts, but purchase them rarely. Put more concretely, 73% of customers would choose Krispy Kreme if they could only eat one doughnut for the rest of their life.2 At the same time, customers visit a Krispy Kreme location less than 3x per year3, and 59% of customers say they don’t choose Krispy Kreme because their locations aren’t convenient.4 There are a few different options to solve this dynamic:

Build locations in better areas. The problem with this approach is better areas mean more expensive real-estate, which is especially challenging for a company that’s trying to reduce leverage rather than increase it.

The second, much cheaper, option is to find a way to work with companies that already have prime real-estate and sell through their stores. This approach doesn’t work if you’re a McDonalds or Starbucks, because you need a kitchen or espresso machine on site. No one wants a Big Mac or latte that was made at 5am and is now cold. It does work if you’re a donut company, and can deliver those donuts daily to grocery/convenience stores and quick-service restaurants.

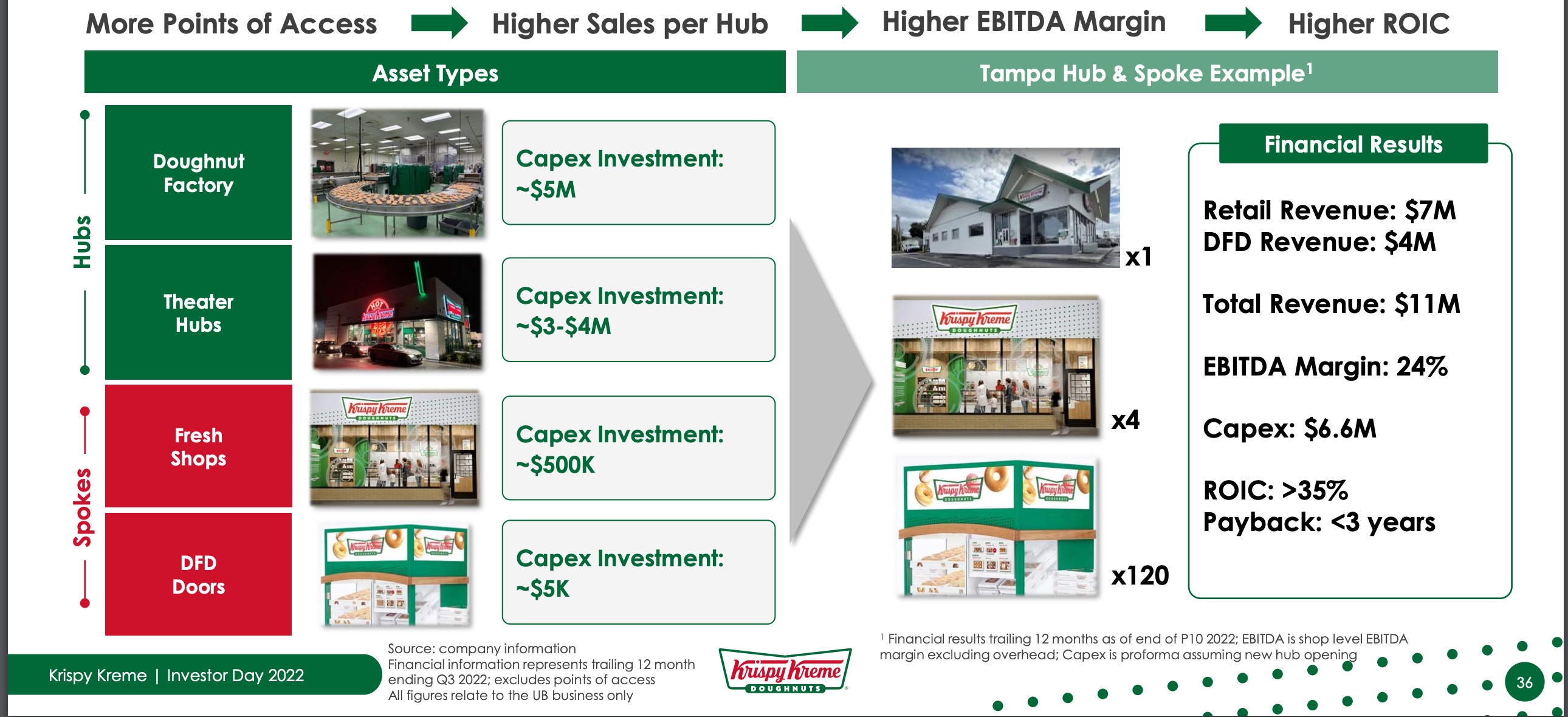

Krispy Kreme ended up choosing a blend of both these options, which it terms the “Hub and Spoke Model”, and is best described by the following slide:

Krispy Kreme has built locations in better areas, but to partially solve the problem of expensive real estate it’s built storefronts with no kitchen, requiring both less square footage and equipment investment.5 The company’s also leveraged the second option, setting up donut display cases in grocery stores, and recently selling through 160 McDonald’s locations in Kentucky.6 Donuts are delivered daily to both Fresh Shops and these DFD locations. This has multiple benefits for Krispy Kreme, but chief among them is achieving significant revenue growth without significant capital expenditures. Lower capex should mean higher margins, and thus higher free cash flow over time. This is a legitimate approach, and management has emphasized there’s significant room for optimization here, whether through merchandizing more premium donuts or improving the donut display cases.7 However, current evidence of margin expansion is impressive but largely anecdotal. EBITDA margins for the Nashville area increased by 1200 basis points when stores converted to the DFD model, and Tampa’s EBITDA margin is impressive, but US and Canada Adjusted EBITDA has been roughly flat from 2020-2022 at around 11.5%.8

The Hub and Spoke model might be capital-light in theory, but it hasn’t been so in practice. While opening DFD doors and Fresh Shops is cheap, part of the process for building out the Hub and Spoke system involved buying franchises back from owners, which required over 450mm in capital as of Q12021.9 This has led to two potential issues: overstated revenue growth and debt. Revenue’s increased by nearly threefold since 2016, but that’s much less impressive given the franchise acquisitions.10

This slide is reasonably misleading. Franchises pay around 3% of total revenue every year to Krispy Kreme, but if Krispy Kreme owns the store outright all of that total revenue gets included in the top line. It would be deeply concerning if revenue hadn’t increased substantially over the time period of absorbing franchises. Current debt levels aren’t necessarily a concern, but the tempo of debt paydown is. Management’s hope was to be at 3.0x net leverage by the end of 2022. Instead, the business ended at 3.9x.11 This is an issue for investors, particularly if one was betting on reduced debt mechanically increasing Krispy Kreme’s equity value.12

Unfortunately, the Hub and Spoke model isn’t the company’s only plan for revenue growth. In the past few years, Krispy Kreme also launched its Branded Sweet Treat Line, acquired a majority interest in Insomnia Cookies, and is currently expanding internationally, hoping to open in 5-7 countries in 2023. This makes it a tricky business to evaluate. Management emphasizes the omni-channel and DFD strategy, but spending on other initiatives obscures whether the strategy is in fact working. If the strategy succeeds, these other growth plans threaten to mute its effectiveness. It’s not hard to envision a failed international expansion, or Insomnia growing stores too quickly, or the Branded Sweet Treat line failing to justify the required investment.13 Any of these scenarios would not only make overall business growth less impressive, but also would mean wasted capex and a slower debt paydown. For these reasons it’s hard to get excited about the Krispy Kreme business, despite a promising Hub and Spoke approach and great donuts.

DFD is short for delivered fresh daily, referring to the Fresh Shops and grocers/QSRs that get daily deliveries of donuts.

Pg 9 of S1.

Slide 27. 2022 Investor Day Presentation

Slide 36, Ibid.

“We'll achieve higher sales per door by focusing on premiumizing our DFD options in the U.S., including adding LTOs this year and upgrading our merchandizing units with more menu choices and better displays. These are improvements that will drive higher sales per door, increase the bottom line and improve margin.” - Q12022 Earnings Call

See 2022 full year press release and 2021 press release. In fairness, Krispy Kreme spent much of 2022 struggling with raw ingredient and wage inflation.

Pg 68, S1.

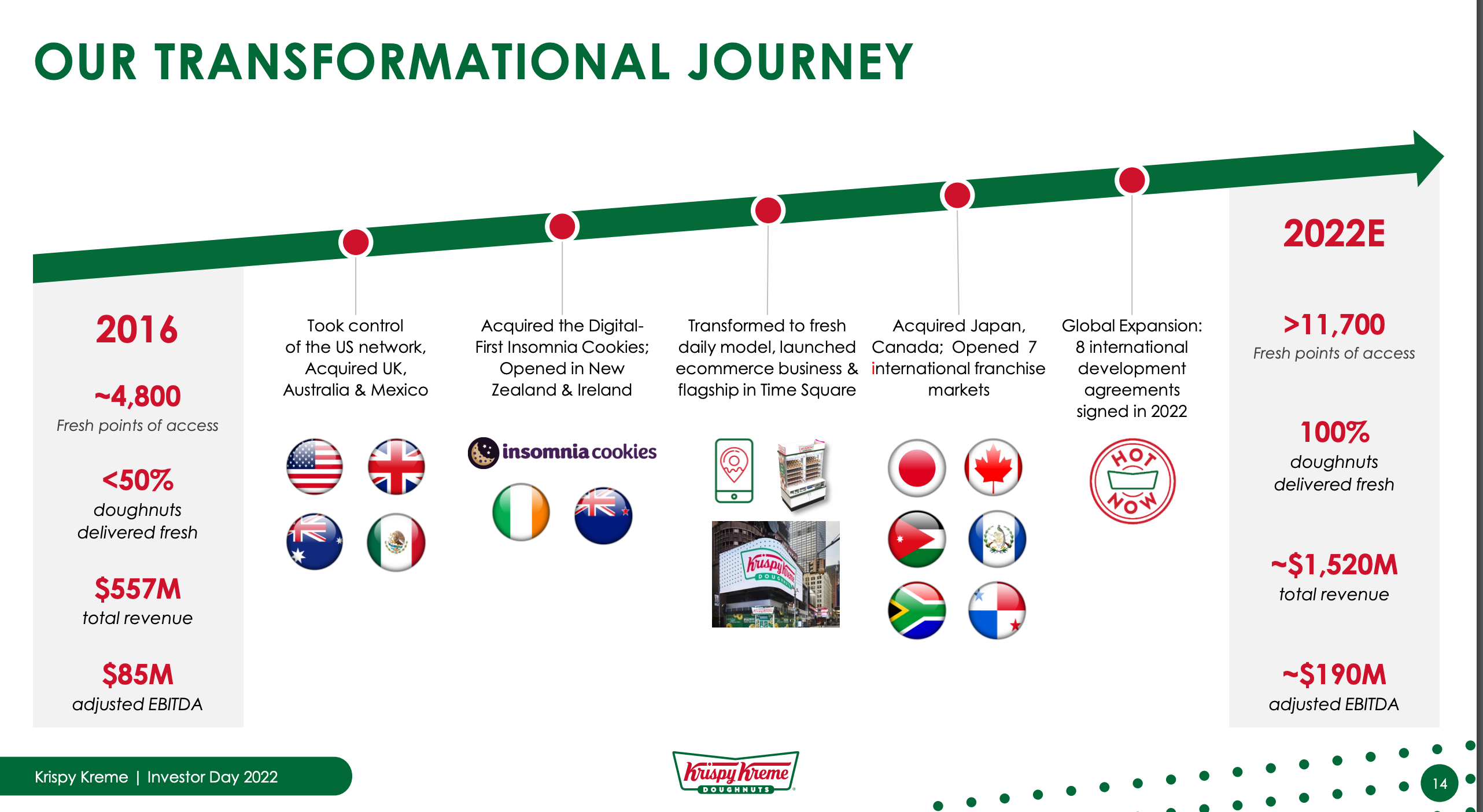

Slide 14, 2022 Investor Day Presentation

See 2022 full year press release

See Verdad’s paper to learn more about the return characteristics of leveraged companies that pay down debt.

This is particularly the case with Insomnia Cookies, which is ramping up to open 100 stores per year.