Lamb Weston: Can a McDonald's French Fry Supplier be like Transdigm? $LW

Thanks to all who are reading this week. Feel free to reach out with feedback, especially criticism!

One of the more entertaining experiences I’ve had reading a 13f filing was finding out that Anomaly Capital’s largest holding was Lamb Weston, a producer and distributor of frozen potato products, most notably french fries. Its business can be broadly split into three different segments:

Global - The top 100 North American restaurant chains, which includes the likes of McDonalds and Chick-fil-A. This business segment is lower margin, but has the dual advantage of being high volume and predictable; it’s much harder for McDonalds to go out of business than a local neighborhood restaurant! The global segment also includes international customers of all types (QSR/full service restaurants, foodservice distributors, retailers), so margins aren’t perfectly representative of how fast food mammoths are doing.

Foodservice - US and Canadian customers that are not part of the top 100 restaurant chains. Think smaller QSRs, full-service restaurants, and commercial distributors.

Retail - frozen potato products sold through North American retailers. This includes Lamb Weston brands like Alexia, but also some retailers’ private potato brand products. Margins for this segment have also predominantly been below LW’s foodservice segment.

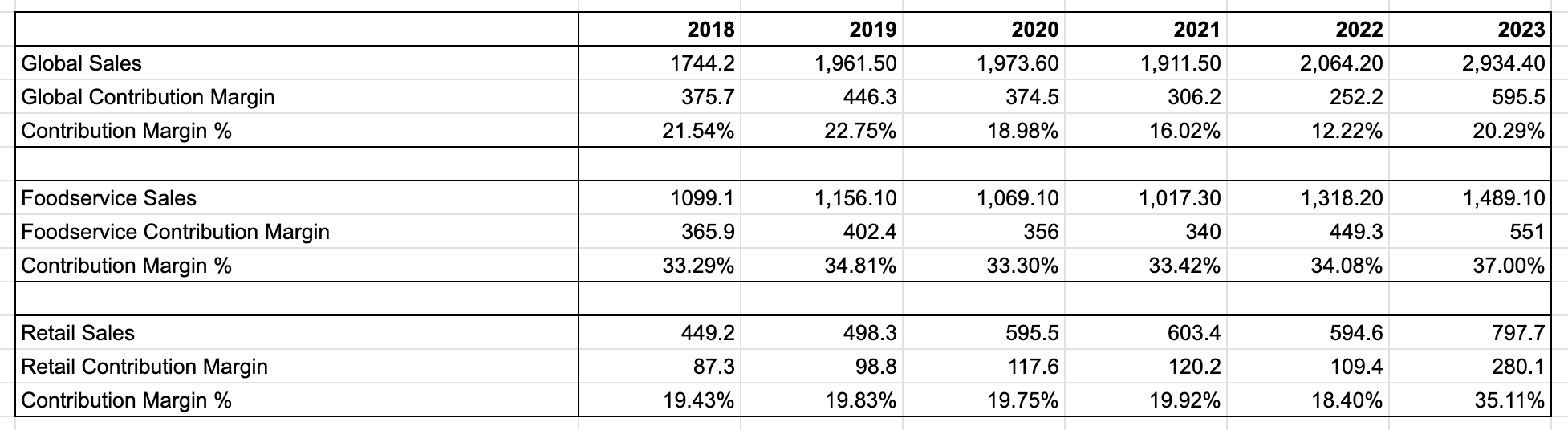

While the company’s reporting is changing going forward, management has previously been transparent about the contribution margin of each business segment, defined as net sales - (cost of sales + advertising/promotion expenses):

The oscillations in segment contribution margin mostly indicate the dangers of being a frozen potato company during a lockdown that happens to coincide with a bad potato crop and other significant input cost inflation. That said, it’s still a useful lens to understand how the segments stack up against each other. The boost in 2023 margins is unlikely to persist, as the potato crop for next year was contracted at prices 20% above 2023 costs in the US and 35-40% above 2023 costs in Europe. The 2018-19 years represent the more typical, steady-state margins one can expect in ‘normal’ years.

The bull thesis for Lamb Weston goes something like this: the company sells a critical component to its customers that makes up a small part of those customers’ overall expenses. This combination leads to a significant amount of pricing power: it’s not a good use of a restaurant’s time to find a new supplier if Lamb Weston increases prices below a certain threshold.1 McDonalds isn’t the same if it doesn’t offer french fries, and yet offering them is incredibly cheap when compared to the cost of beef, chicken, and labor. Consequently, LW’s margins and earnings are currently understated relative to where they’ll be in 1-2 years, so the stock’s a buy. Importantly, this thesis assumes that product volumes stay reasonably consistent; margin expansion matters less if sales are trending down!

Readers who have studied a certain aerospace parts manufacturer may realize that the above paragraph sounds similar to what the bull case for Transdigm would’ve been ten years ago. In that case, the thesis played out so well that the company was subject to a congressional hearing on price gouging.2 Transdigm provides essential components for aircrafts that make up only a small part of a plane’s overall cost. As a result, the company can, for the most part, periodically raise its prices without worrying that Boeing or Raytheon will balk and go find another supplier.3 Transdigm’s stock chart gives some indication as to how this strategy worked over time:

I think there are more differences between Lamb Weston and Transdigm than the bulls appreciate, and that the pricing power thesis may not play out as hoped. Potatoes make up a small percentage of McDonald’s overall cost, but they don’t make up a small percentage of McDonald’s executives’ overall brain space. French fries are a software-like margin item for the business, and an item that the chain sells 3.29 billion pounds of every year. It’s almost irrelevant that they make up a small portion of COGS when they’re such a fundamental part of what McDonalds offers. This stands in contrast to a Boeing or Raytheon where, until recently, it’s unlikely that executives were devoting much time to considering whether they were overpaying for parts that constitute a tiny part of the final product. Parts that, importantly, aren’t a key part of a strategy to boost the company’s overall margins.

There are two counters to the above point: the first is that Lamb Weston has taken up prices over the last few years in response to both temporary and more permanent pricing pressures; once these temporary pressures subside the company will leave its price increases in place, and so reap higher gross margins. For example, Lamb Weston experienced a historically poor potato crop in 2021, which necessitated open-market potato purchases that are more expensive than contracting with farmers at the beginning of the year. Assuming this year’s crop is more typical, margins should get a nice lift. Unfortunately, management has already indicated that a normal crop yield won’t lead to margins above guidance.4 I’m also skeptical of this line of thinking for another reason, which is that McDonalds and other big chains are unlikely to let their suppliers permanently benefit from non-permanent pricing pressures. Walmart has spoken on recent earnings calls about re-negotiating prices with its suppliers who experienced deflation coming out of 2022, and it seems reasonable to assume that large restaurant chains would do the same. The second counter to the above paragraph is that McDonalds and other behemoths have less bargaining power with Lamb Weston than one might think given the frozen potato producer market structure in the U.S. It’s not an easy task to supply massive QSR restaurants with all the french fries that they need, and there are only four companies in America that are plausibly able to do so.5 McDonalds can try to play hardball with Lamb Weston, but the reality is it’s far from a simple task to swap out suppliers. I’m open to this line of thinking being correct, but it’s equally not clear that Lamb Weston wants to walk away from what is essentially high volume, recurring revenue that deserves a higher multiple than its Foodservice segment. There’s a reason investors generally prefer enterprise SaaS companies to those that serve SMBs! Nor can the company easily replace revenue from a customer that contributed 695mm to its topline in fiscal 2023. The potato producer’s volume dropped 8% last quarter as compared to this time last year, driven primarily by exiting four different lower-margin contracts. Management’s hope is to backfill this volume with higher-margin customers, but has emphasized that the sales process to return to those previous levels doesn’t happen overnight. Given the substantial portion of revenue that large restaurant customers constitute for the company, and the length of time it would take to backfill this lost volume, it’s unlikely that executives would walk away from these large deals unless there were intractable disagreements on pricing. Improvements in margins mean much less if it leads to substantial churn along the way! Furthermore, there’s a competitive advantage that comes from serving what are likely the most demanding players in the restaurant industry. Miles Grimshaw has discussed, although in the context of startups, the importance of having customers that pull forward the quality of your product:

“Stripe early on, for example, didn't go and get Bed Bath & Beyond or Best Buy as customers. They got Lyft and they got Instacart and they got DoorDash, and those customers were the market-leading ones. They were pushing the future forward and then were going to pull Stripe along with them, and Stripe would have to keep up and adapt its needs.”6

This isn’t a philosophy helpful only to startups. It’s always advantageous for businesses to serve customers that raise their quality bar higher. “We serve the world’s most tech-forward companies” isn't only marketing fluff in a sales pitch; it’s an indication that a company can serve its most sophisticated customer segment.7 Similarly, “We serve the world’s largest QSRs” is a signal not only that Lamb Weston can handle a lot of volume and likely delivers close by to your restaurant’s location, but also a signal that the product meets a certain product bar.

Of course, Lamb Weston doesn’t only serve behemoths. Another portion of its customer base is smaller restaurants that pay sticker price rather than institutions with real bargaining power. But the issue with overly raising prices on this segment is that smaller restaurants are, well, smaller. Increasing prices on these customers can work during good times, but in leaner times there’s a real risk that these businesses simply can’t afford the proposed price increases. Over the past decade Google benefited from not only having many small customers who were price-takers, but also from having many small customers that were venture-backed and flush with cash; that same dynamic doesn’t exist in a self-funded industry with notoriously thin margins.

This leads into a related point, which is that a bet on Lamb Weston’s margin expansion is also a bet on the macroeconomic outlook. While the economy on the whole has held up better than expected, the company has repeatedly emphasized on recent earnings calls that U.S. traffic has been shifting away from full-service restaurants towards QSRs. In other words, shifting from a higher-margin business segment to a lower one. This complicates the Lamb Weston bull-thesis from ‘the business has latent pricing power which will lead to margin expansion’ to ‘the business has latent pricing power which will lead to margin expansion assuming there’s not a downturn that overly shifts traffic to QSRs.’ The second thesis is a harder one to predict than the first! A downturn in the European market would be especially harmful to the bull case, as far fewer drive-thru locations means traffic instead shifts away from full-service restaurants to eating at home.

The final argument I’ve heard in favor of LW’s margins increasing over time circles back to the market structure of the US frozen potato processor industry. In contrast to Europe, the US is essentially an oligopoly, and industry players are very transparent when they plan to bring on additional french fry/potato product capacity. Assuming these oligopoly players want to maintain or increase their margins, they’ll slightly underbuild supply relative to demand. Put another way, they’ll act like the U.S. oil industry today rather than the oil industry in 2014. In this scenario McDonald’s bargaining power is significantly weaker, resembling something closer to hyperscalers’ current position with Nvidia. This claim isn’t uncontroversial, and is partially hard to evaluate because the other dominant U.S. frozen potato companies are all privately held. A Lamb Weston short-seller from 2019 argued that these players want to win at any price, but even if that’s not the case it’s unclear that the supply/demand dynamics are what bulls think they are. The most worrying evidence of this comes from Lamb Weston’s recent investor day, where demand outstripping supply isn’t seen as a sure bet:

There are, as with most companies, other possible paths for Lamb Weston to outperform. Europe, which the company has recently expanded into via acquisition, is a market with much lower margins, but sales growth in that region could grow better than expected. The macro environment could also markedly improve, shifting volume towards full-service restaurants who are then more receptive to pricing increases. Management has expressed a desire to shift product mix towards higher-margin, batter coated french fries, but such a shift requires additional capex, is more volume constrained, and won’t occur overnight. For now, though, the company has a few headwinds to overcome beyond only macro and pricing concerns: SG&A expenses have been higher than analysts expected due to an ERP implementation and are expected to stay that way through 2026. Capex is also trending higher and won’t peak until 2025, perhaps making the stock less of a bet on latent pricing power and more of a bet on management’s growth initiatives.

Disclaimer: The information in this post is not intended to be and does not constitute investment or financial advice. You should not make any decision based on the information presented without conducting independent due diligence.

Will Thorndike, author of The Outsiders, has a 3-part podcast series on Transdigm that can be found here.

From the Q124 earnings call: “Just a reminder, our cost and contract raw input structure is baked. So, wherever the crop yields and all that comes out, it really isn't going to impact our overall input cost for the balance of this fiscal year…..you're not going to see any, any decline in our cost structure, because the crop is great. It's just we have agreed to a contract last year ago and it is what it is.”

Lamb Weston’s dominant competitors, all privately held, are J.R. Simplot, McCain Foods, and Cavendish Farms

John Collison mentioned this in a recent ILTB interview that can be found here: “When we go and talk to the CIO of some giant retailer or some large manufacturing company or something, the fact that we're working with actually the world's most innovative, at least new companies, is a very strong kind of positive in their eyes……they want to hear what are the upstarts doing so that they can go and roll it out themselves.”