MaxCyte: Trading at less than book and then some $mxct

Casgevy, In-vivo, SeQure Dx

I wrote about MaxCyte (disclosure: long), a provider of electroporation instruments for manufacturing ex-vivo cell/gene therapies, back in September. Since then, the stock is down almost 50%, and nearly 80% from this time last year.

The company’s business model is simple: sell/rent instruments to academic/research customers, rent them out to any customers developing therapeutics, and then enjoy milestone/royalty payments on top of that lease revenue. MaxCyte counts CRISPR Therapeutics/Vertex as customers, who co-developed Casgevy, the first (and only) FDA-approved therapy leveraging CRISPR.

There are a few plausible reasons MaxCyte has been hit so hard over the past 5 months:

The Casgevy launch hasn’t been a homerun thus far. To be sure, there’s significant logistical complexity to delivering an ex-vivo gene therapy around the world. But the anemic start has led to questions on what the appetite for these one-time therapies really is.1

There’s been a shift in sentiment/funding away from ex-vivo cell/gene therapies and towards in-vivo. MaxCyte’s instruments aren’t needed for manufacturing in- vivo therapeutics.

There’s probably some forced selling from funds that won’t hold stocks with a sub 100mm market cap or sub $1 price.

There was definteily some forced selling after MaxCyte was dropped from the Nasdaq Biotechnology Index in late December.

These headwinds are on top of a 2025 that was already looking disappointing. Customers cut the number of programs in the pipeline/went under altogether, there was general instrument purchasing hesitancy, and two large customers streamlined manufacturing in such a way that reduced the number of electroporation instruments required.2

As a result, MaxCyte has gone from trading at an incredibly frothy valuation when it listed on the Nasdaq back in 2021 down to trading at less than 0.5x tangible book value.3

This seems like a bit of an overreaction for a company providing an essential instrument for the manufacturing of a therapeutic. In most cases, if there’s no electroporation then there’s no way to get the gene-editing complex (whether CRISPR or otherwise) into the cells non-virally.4 If MaxCyte’s instruments disappeared tomorrow Casgevy’s revenue would drop to zero. Vertex/CRISPR Tx would have to go through a lengthy process of validating a different electroporation instrument, in addition to a rigmarole with regulatory bodies across various countries.

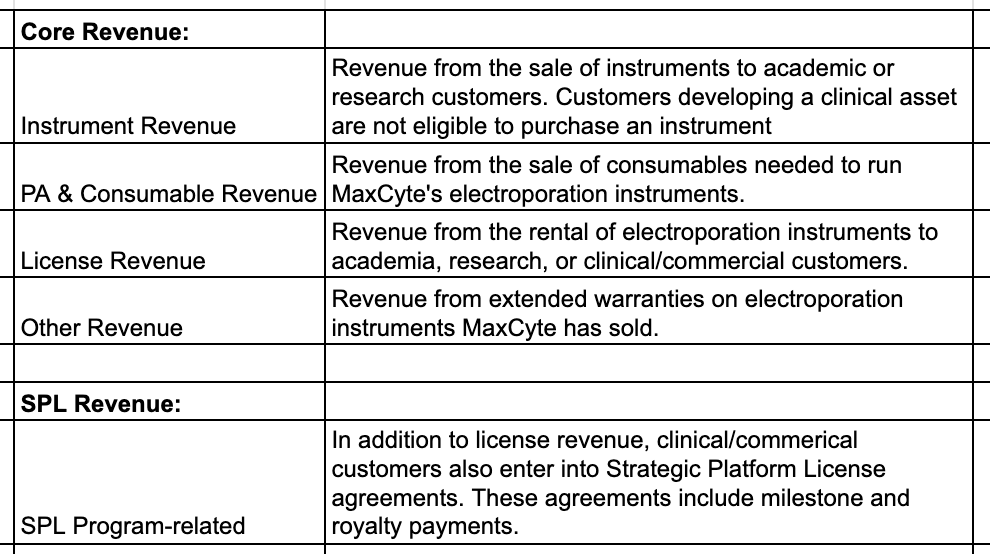

These are MaxCyte’s individual revenue segments:

The ‘Core Revenue’ portion of the business has two attractive characteristics: low churn and a high percentage of recurring-ish revenue (~75% of ‘24 core revenue was licenses or consumables). That’s not to say it has the characteristics of an enterprise software business. Many of MaxCyte’s customers operate with plenty of science risk, and if ex vivo gene-editing approaches don’t take off the business will be in a challenging spot. Having said that, once a clinical company starts using a MaxCyte electroporation instrument, churn is very unlikely. Much like clinical testing companies using Illumina, switching providers creates massive workflow and regulatory headaches.

The SPL portion of revenue is frustratingly lumpy and carries with it a good amount of uncertainty. If a company fails in phase 1 clinical trials and folds its ex-vivo program(s), then the value of the related SPL agreement goes to zero. That said, the revenue that could come from these agreements is 100% gross margin, and a critical part of making the MaxCyte business model work. Management does have a reasonable amount of visibility into how many SPL agreements will be signed every year. The company is often working with these customers in the early research phase of developing a clinical asset, and so has a good sense for which of these customers are preparing to submit IND applications. MaxCyte expects to sign 3-5 such agreements in 2026.

Casgevy is a decent illustration of how MaxCyte’s business should ideally work. MaxCyte and CRISPR Therapeutics signed their initial agreement in March 2017. As Casgevy progressed through clinical trials there were milestone agreements along the way (in the mid-6-figure to 7-figure range). Management is cagey about breaking out SPL revenue by customer, but the 8.5mm in SPL revenue back in Q423 was likely all related to FDA approval of Casgevy. Going forward, MaxCyte will collect royalty payments that are ~1% of Casgevy sales, on top of instrument leasing/consumables revenue.

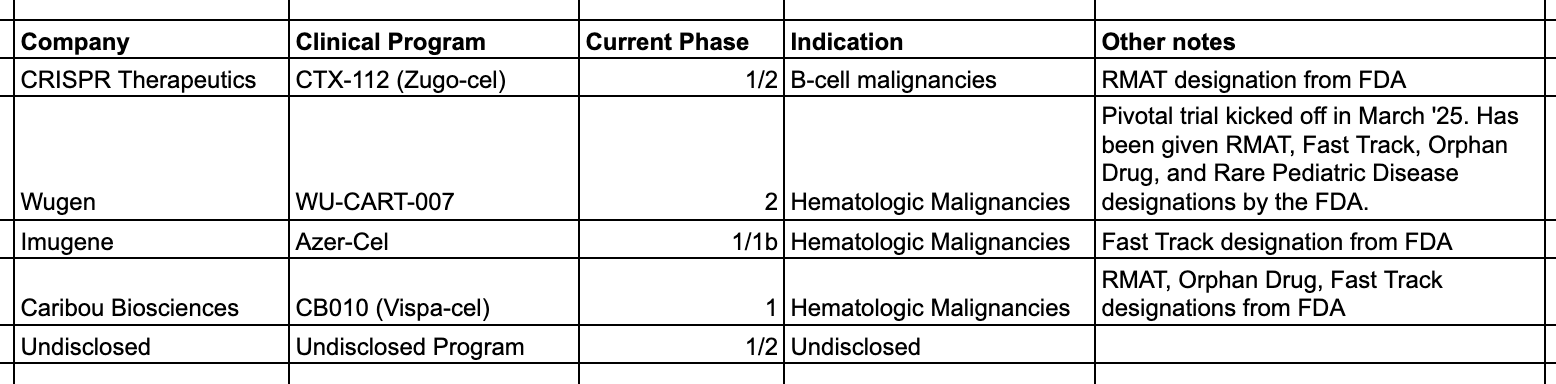

Here are the 5 programs MaxCyte expects to enter pivotal studies in the next 6 – 18 months:

There are a few things worth flagging here. Most notably, both Caribou and Imugene need to raise additional capital to carry out their pivotal trials. That’s extra challenging when pharma companies and investors are more excited about in-vivo than ex-vivo. I think the undisclosed customer program in Phase 1/2 trials is Beam’s Risto-Cel candidate for severe sickle-cell disease. In some ways this isn’t the most attractive asset for MaxCyte to have in its portfolio. Risto-cel would be a direct competitor to CRISPR/Vertex’s Casgevy, and so doesn’t really grow the pie of potential royalty sales.5 That’s true, but the other way of looking at it is MaxCyte gets twice the milestone revenues for treating the same indication.

MaxCyte is trying to diversify beyond just electroporation instruments/consumables, as seen with the company’s acquisition of SeQure Dx last year for $4.5mm in cash. SeQure Dx provides off-target analysis services for in-vivo and ex-vivo cell/gene therapies; it’s an early-stage business, expected to bring in ~2mm in revenue for 2025. At least part of the goal here is to shift the business away from existing only as an index on the growth of ex-vivo cell/gene editing therapies. I don’t have all that substantive of an analysis to offer on this acquisition, but I would note that the acquiree’s services were used in the development of the N of 1 CRISPR therapy for baby KJ that was (rightfully!) so heavily publicized. This also means the FDA evaluated the off-target analysis done by SeQure Dx, and was comfortable enough with the results to give the go ahead. Biopharma companies tend to like using tools that the FDA is already familiar with, and probably especially so in a more nascent field where there’s already a good number of unknown unknowns.

It’s certainly true that there’s been a sentiment shift away from ex-vivo approaches towards in-vivo. However, companies like CRISPR and Beam have been quite transparent that in-vivo has always been where they’ve hoped to eventually go. That hasn’t stopped them from putting capital behind ex-vivo approaches, and remaining excited about these approaches at the most recent JPM Healthcare Conference:

“We’re looking at 4 to 6 months for the entire journey to potentially cure yourself of sickle cell disease. So clearly, we believe this would be very attractive and bode well for Ristacel’s uptake within the market. But in fact, we think we can actually grow the market because you can use an existing amount of clinical infrastructure and potentially with numbers like these, treat more patients. So we’re very excited about the potential of the program and its differentiation” – Beam CEO John Evans

“In oncology, here are the baseline characteristics, very severe patients, all high risk, several primary refractory, all with SPDs above 2,000 millimeter square. And in these patients that are very sick, that -- many of them have actually gone through T-cell engager therapies and not responded, one even went through an auto CAR T before and then they were treated with zugo-cel and they had complete responses. This is remarkable. I don’t think there’s any other allogeneic therapy out there that has shown responses after auto CAR T.” - CRISPR CEO Samarth Kulkarni

Not exactly the nail in the coffin for ex-vivo! On the big pharma side, there have been a lot of recent acquisitions on the in-vivo side of things (AbbVie bought Capstan, Gilead bought Interius, and BMS bought Orbital). Eli Lilly bought Orna a bit over a week ago, but also recently announced a collaboration with CRISPR Therapeutics evaluating zugo-cel with pirtobrutinib in aggressive B-cell lymphomas. Again, not exactly a nail in the coffin.

None of this is to say that MaxCyte hasn’t run into problems recently, and few people would argue the company’s ‘21 valuation was justified. Moreover, the business isn’t profitable, which makes current headwinds harder. I gave a rough outline of the MaxCyte/CRISPR Therapeutics agreement earlier, which illustrates how the business model works and highlights its challenges. A 1%-ish royalty agreement means the therapeutic has to perform well to be of real value to MaxCyte, and that a lot of the company’s terminal value is wrapped up in revenue far out in the future. Consequently, the slowdown/culling of early-stage ex-vivo clinical programs has implications for the business beyond just some foregone instrument revenue.

I don’t dispute any of this, but I’m not sure the appropriate response is for the company to be valued at <0.5x tangible book. Management reduced headcount and expects cash burn of 10-15mm for next year. Cash/cash equivalents/short-term investments sat at 105.7mm as of Q325, and the company has no debt, so is unlikely to run out of money/default in the short-term. Its business model involves a lot of selling consumables and licensing instruments. In other words, high-margin activities. These activities bring with them the potential for milestone/royalty payments, which are even better than high margin. Very importantly, their customer base includes companies that are real trail blazers in the cell/gene therapy space. Over the past year, ~97% of insider buying/selling has been buying. The executive team is well-paid, but over 70% of the CEO’s comp is in the form of stock/options, which is presumably fairly motivating.

There is, of course, plenty I could be wrong about. There’s always science risk, and MaxCyte having a broad portfolio of customers doesn’t mean it’s not possible that Casgevy’s the only program that pans out. Alternatively, maybe a few do pan out, but don’t hit enough of a commercial ramp to be of real value to the business. Maybe many pan out but then are beaten out quickly by emerging therapeutics with better efficacy. There are no guarantees with biotech tools suppliers!

Disclaimer: The information in this post is not intended to be and does not constitute investment or financial advice. You should not make any decision based on the information presented without conducting independent due diligence.

This concerns have perhaps somewhat abated after Vertex’s Q4 earnings, when it was reported that 30 patients received Casgevy infusions, up 3x from Q3.

It turns out there are real downsides to having two cell therapy companies account for 32% of revenue and five companies account for 46% of revenue (accurate at least as of MaxCyte’s 2024 Annual Report, pg 39).

MaxCyte initially went public on LSE’s AIM exchange in 2016. The company has since delisted from there.

Intellia Therapeutics is working on an ex-vivo delivery method that doesn’t require electroporation.

Beam would slightly disagree with this, arguing that their approach is superior and so actually grows the total addressable market.